It’s never been more important to understand your cashflow

17 January 2022

The COVID-19 pandemic has left many manufacturing firms short on cash. Manufacturing Advisor Martin Hyman explains why ‘cash is king’ in business, shares some tips on how to improve liquidity and outlines the cashflow risks every business needs to be prepared for.

Turnover is vanity, profit is sanity, but cash is king. That’s a saying worth remembering, and since the COVID-19 pandemic it’s been truer than ever.

Many businesses are now dealing with what economists call a ‘liquidity squeeze’ or ‘credit crunch’ where cash is increasingly difficult to come by. Companies have been hit by a combination of irregular revenues due to economic disruption, the burden of new debts such as Bounce Back Loans, a sharp increase in prices, and suppliers and customers doing all they can to hold onto their money.

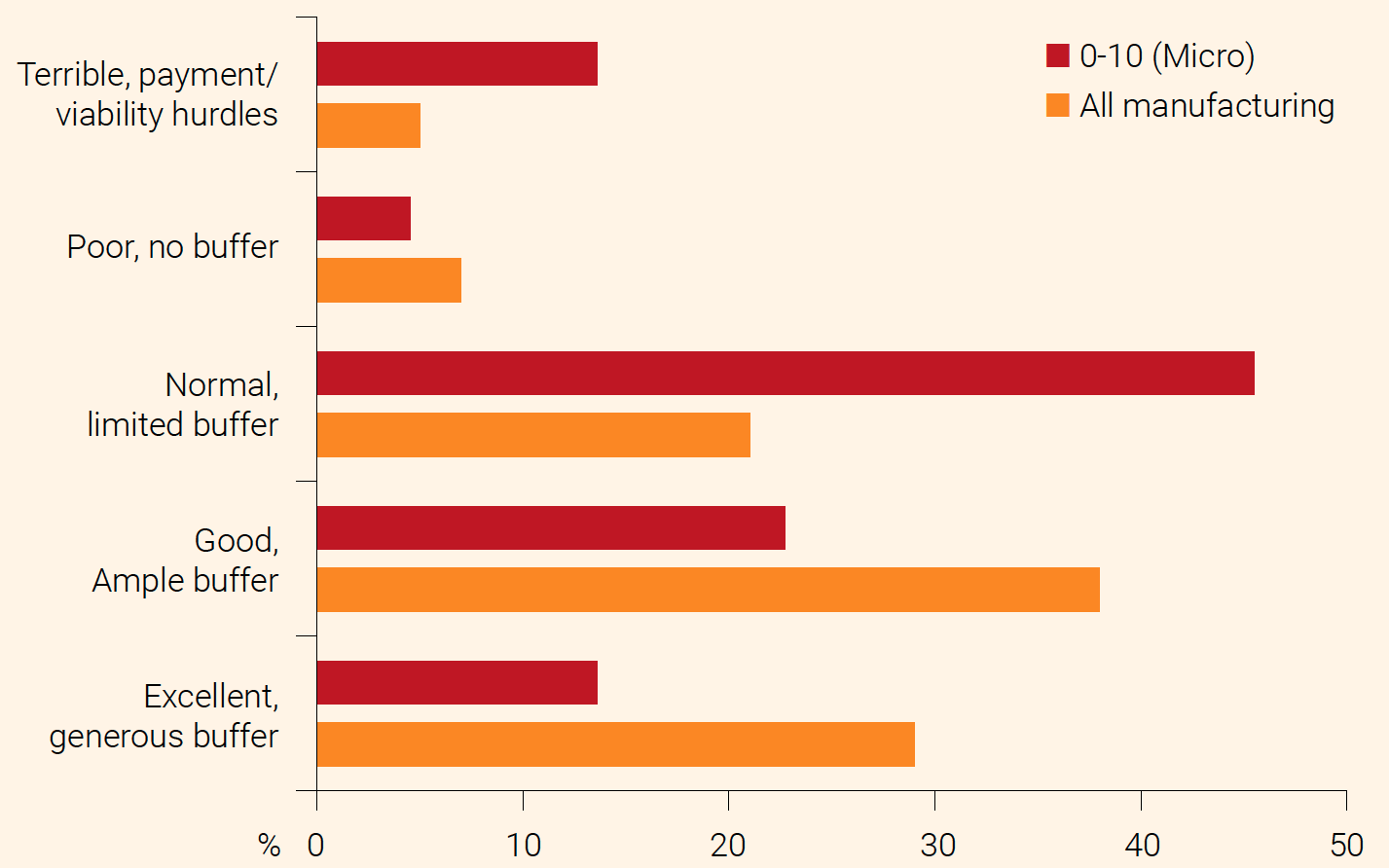

According to the manufacturers’ organisation Make UK, around half of manufacturers ended 2021 with a worse cash position than at any time since the beginning of the pandemic. The smaller the business, the worse the situation tends to be.

How manufacturers described their cash position in 2021. Sourced from Make UK and RSM Survey, October 2021

Why cash is king

Running out of cash is the number one killer of small businesses. This is because companies tend to focus on chasing turnover and profit on the assumption that growing sales always means a healthier business. Turnover and profit are important, but it’s cash that really matters, and here’s why.

Let’s say you sell £100,000 of goods that cost you £75,000 to provide. You need to pay out these costs immediately but won’t get paid yourself for 30 days. This means you have a cash shortfall of £75,000, even though you have made a profit of £25,000. If sales remain static the situation will improve over time, although it will still take several months before you have real cash in the business.

|

Month |

Sales (£) |

Profit (£) |

Cash In (£) |

Cash Out (£) |

Cash in Business (£) |

|

1 |

100 |

25 |

0 |

75 |

-75 |

|

2 |

100 |

25 |

100 |

75 |

-50 |

|

3 |

100 |

25 |

100 |

75 |

-25 |

|

4 |

100 |

25 |

100 |

75 |

0 |

|

5 |

100 |

25 |

100 |

75 |

25 |

Now consider what happens if sales double each month. Sales and profit are flying, but your actual cash in the business just gets worse and worse.

|

Month |

Sales (£) |

Profit (£) |

Cash In (£) |

Cash Out (£) |

Cash in Business (£) |

|

1 |

100 |

25 |

0 |

75 |

-75 |

|

2 |

200 |

50 |

100 |

150 |

-125 |

|

3 |

400 |

100 |

200 |

300 |

-225 |

|

4 |

800 |

200 |

400 |

600 |

-425 |

|

5 |

1600 |

400 |

800 |

1200 |

-825 |

This is called ‘overtrading’ – you are buying more and more stock to sell to more and more customers, but in doing so you run out of operating cash or ‘working capital’ (your current assets minus your current liabilities, in accountancy speak).

It’s operating cash that pays your bills and expenses, not revenue or profit. The longer your cashflow (the flow of cash in and out of the business) remains negative, the harder it gets to pay your bills, and eventually you go bust.

Getting access to cash

So how do we solve this problem? Measures need to be taken to ensure a sufficient level of ‘liquidity’ in the business, or in other words, the ability to access cash whenever you need it. Some of the options available include:

Payment terms

Negotiating shorter payment terms with customers (or longer payment terms with suppliers) will help to close the gap between cash in and cash out. According to Make UK’s research, nearly half of manufacturers changed their payment terms in 2021 to improve their liquidity.

Just over a third of companies even started blocking customers who fell afoul of their payment terms, thus sacrificing potential future sales to preserve their cash. Staged payment schedules may also be useful, and you could even offer a discount in return for early payment.

Consignment stock

Using consignment stock means your supplier retains ownership of stock until it is sold or used, so you only need to pay once the sale goes through, not when you take possession of the stock. In other words, it shifts the costs of carrying inventory from the buyer to the supplier. This is a common practice in industries that involve high value items or longer sales cycles, and it can be particularly useful during times of uncertainty.

Invoice finance

Invoice finance can help to overcome cash shortfalls by providing immediate payment on invoices. Effectively, an invoice finance provider will lend you most of the outstanding value of an invoice as soon as you issue it, giving you instant access to the cash you need. The loan is then repaid with interest once you receive payment from your customer (this is also called invoice discounting). Alternatively, there is invoice factoring, where the provider purchases your invoice outright and takes over the responsibility of collecting the debt from your customer.

Risks to monitor

It’s amazing how many small businesses run out of cash simply by not monitoring their cashflow. My number one piece of advice to every business is to track and forecast cashflow using a modern accounting system, so you always know how much cash you have in real-time and when any shortfalls are likely to occur.

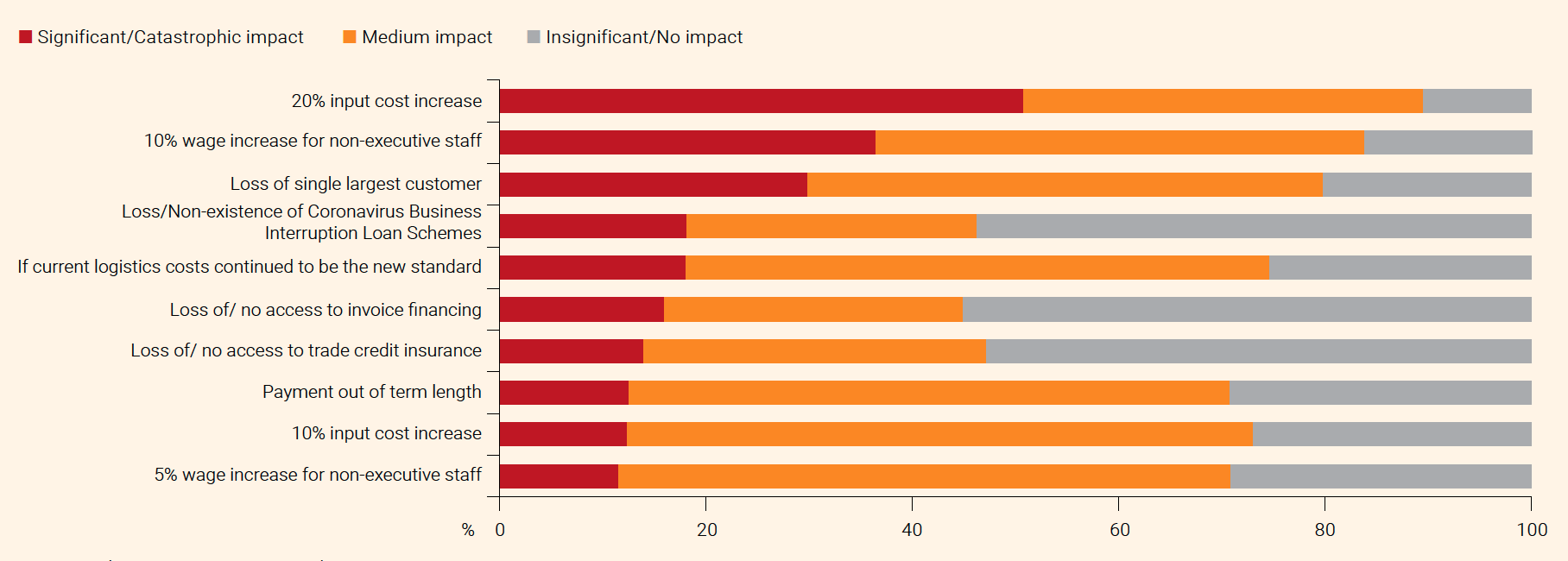

You also need to understand how your cashflow might be influenced by external factors. Make UK’s research shows that rising input costs were the biggest perceived threat to manufacturers’ liquidity in 2021, followed by wage increases and the loss of a key customer.

How manufacturers ranked different threats to cashflow in 2021. Sourced from Make UK and RSM Survey, October 2021

The risks to your cashflow are endless, but here are some of the key issues to keep an eye on:

Input costs

Now that we’re recovering from COVID-19, rapid price inflation has put severe pressure on many businesses. You can manage rising material costs by being as efficient as possible with materials you use, agreeing long-term pricing deals, or stockpiling at today’s prices if you are confident that they will continue to rise.

If possible, it may be worth considering switching to a lower-priced, more accessible alternative that provides the same material properties. In some cases, it may even be possible to negotiate free issue raw material, whereby the customer provides the material you need free of charge, so you only pay for the labour cost of producing the final product.

Productivity and inventory

Any form of waste in your business is an unnecessary cash burden. Managing the 8 Wastes through lean manufacturing techniques will improve productivity and free up more cash. Holding inventory is a great example – excess stock may look great on a Balance Sheet, but it isn’t cash; you cannot use it to pay your bills!

Overheads

Overheads such as rent, internet and utilities are all necessary expenditures, but they can quickly get out of hand if not monitored. It’s worth writing down all your overhead costs, item by item, and identifying spend that needs controlling. Sometimes it can be as simple as switching service provider.

The cost of energy may be a particular priority for some manufacturers. In 2021 the cost of gas quadrupled, causing a knock-on spike in power prices that saw energy bills rocket. Our Resource Efficiency Team offers fully funded efficiency audits that will identify ways you can reduce your energy bill.

Salaries

Small businesses often make the mistake of failing to consider all of the costs when deciding to employ new staff. Before adding personnel, ensure your cashflow can cover not just the cost of wages but also all the legal requirements (National Insurance, pensions), as well as salary inflation from minimum wage rises or competition in the jobs market.

Development delays

Development delays on new products can be a cashflow killer, especially if you have spent heavily on R&D. This is exactly what happened to Rolls-Royce in the 1970s when a new engine technology it was developing failed. Orders couldn’t be met, cash ran dry, and the company had to be bailed out by the government through nationalisation of the useful portions of the business under a new government-owned company named Rolls-Royce (1971) Limited. So make sure you have a cash buffer in place and remember to use R&D tax credits where possible.

Customer risk

Always be prepared for the possibility of customers going into arrears or defaulting on payments. One way to protect yourself is to credit check your customers and use trade credit insurance (such as invoice insurance) so you’re not left in the lurch if they go bump.

Capital expenditure

Never lose sight of the need for cash when making purchases. It’s often wise to use asset-based finance for large investments, even if you have enough cash available to pay upfront. You should also think twice about whether you need the purchase in the first place – will it bring in cash or is it just something you want? You’d be surprised how common it is for companies to go under just by spending too much on things they don’t need.

Credit

Borrowing large amounts of money may prevent you from running out of funds in the short-term, but it only delays a potential financial crisis in the future. You should only borrow money after completing a thorough cashflow analysis that proves you can afford the repayments.

During the pandemic, most manufacturers have taken up the option of at least one of the government’s support schemes (such as a Bounce Back Loan). As of 2021, around a third were worried about their viability over the next two years due to new and existing debt. If you’re worried about your debt liabilities, speak to our Access to Finance Team.

Pricing

When is the last time you reviewed your pricing? Are you selling at a profit, or at a loss to win margin? Profit isn’t the same as cash, but if you never sell at a profit, you’re never going to have enough money in the bank. Make sure your prices are actually making you money by measuring all the costs involved in manufacturing and shipping and continually feeding them back into the quotation process. Don’t forget to take inflation into account, as well any costs involved with payment methods or using foreign currency.

HMRC

If there’s one organisation you don’t want to default on, it’s the government. Lots of small businesses mistakenly see all cash as immediately spendable and fail to plan for the cost of Corporation Tax and VAT at year-end / quarter-end. Use a tax calculator to forecast your liability and build up a separate savings pot so you can always pay your tax on time.

Unexpected expenses

If COVID-19 has taught us anything, it’s to always maintain a ‘rainy day’ cash buffer in case of emergencies. Maintaining a comprehensive risk register is a good way to understand all the possible internal and external events you need to protect against. It’s also worth keeping a pot of cash aside to cover equipment breakdowns and maintenance costs.

Get help before it’s too late

If you feel your business is going to run out of cash, the most important thing is to seek professional help.

Our Manufacturing Team can support you in a variety of ways, whether it’s a productivity audit to identify ways to free up cash or tailored guidance to incorporate cashflow considerations into your decision-making.

Martin Hyman, Manufacturing Advisor

Martin leverages the skills and knowledge gained from over 38 years’ experience working in and supporting aerospace, aviation, engineering and manufacturing companies, to now assist Business to Business (B2B) manufacturers across a broad range of Sectors, to achieve their development and growth ambitions.

He works with Company Owners, Directors and Senior Management teams, to understand their needs and ambitions, diagnosing and identifying areas for improvement across the areas of Finance, Manufacturing Strategy, Marketing, New Product/New Process Introduction, Operational Efficiency (KPIs/Lean/5S Principles etc), and Supply Chains, as appropriate.

To view Martin's full profile including technical capabilities and industry experience, please click here.